Investment Thesis

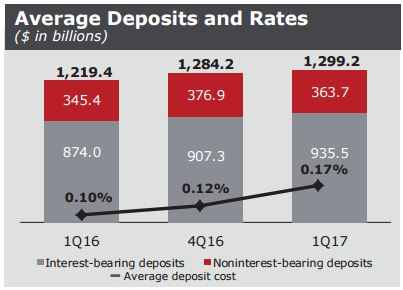

Wells Fargo (WFC) franchise is founded on its the vast and low cost deposit base, its prudent lending practices and its superior non-interest fee revenue streams. Wells is one of the top 3 deposit takers in the US with 10% market share with average deposits of $1.3 trillion at the end of Q1’17 at the average cost of 0.17% p.a..

Wells has shied away from complex investment banking business and was therefore able to keep its loan book simpler than its competitors, thus able to manage credit quality risks during ’08 financial crisis and acquire Wachovia at attractive valuations.

Unlike its major competitors, Wells is not a top player in the capital markets. Its business model is more akin to regional banks than to money center institutions. Wells eschews investing banking and trading and instead relies on the more stable revenue generated by its community and SME banking, brokerage, advisory, and asset management businesses.

Wells is able to generate 30% more revenue per dollar of assets than the same peer group. We attribute this low-cost funding to a loyal base of long-time customers and Wells ability to cross sell multiple financial products, creating sticky and deep relationships with the customer base.

Wells’ successful model, we believe, is well positioned to thrive in the future, as Wells digitizes its operations, allows customers to manage money more conveniently and deploys much needed technology to remain competitive in the face of emerging competition in digital payments, peer-to-peer lending, and robo-advisory investment management services.

| Competitive Advantage | Durable |

|---|---|

| Fair Value Estimate | $43.00 - $54.00 |

| Stock Price | $53.89 |

| Consider Buying Below | $34.40 - $43.20 |

| 52 Wk range | 59.99- 43.55 |

| Market Cap. | $275.1bln |

| Volatily | Medium |

| Balance Sheet | |

| Shareholder Equity | $180bn |

| ROE (%) | 11.1 |

| Net Debt | N/A |

| Debt/EBITDA | N/A |

| Potential Appreciation | 0%-10% |

| Dividend Yield (%) | 2.82% |

| PE Data | |

| 2016 | 13.8 |

| 2017 | 13.0 |

| 2018 | 12.0 |

| 2019 | 11.1 |

$1.3 trillion of low cost deposits at 0.17% cost p.a.

$2 trillion of Assets, ROE targets 11%-14%

70mln+ Customers

Latest developments

Wells made a mistake of having a wrong sales incentive system in place which has resulted in “system gaming” and widespread fraudulent account opening practices. Top management hasn’t acted and paid the price after John Stumpf was replaced as CEO by Tim Sloan and over $100mln of compensation was clawed back. Wells reputation suffered, however we don’t believe that long-term earning power of the franchise is impacted.

In June the Federal Reserve raised its target for the federal funds rate by 25 basis points to 1.0%-1.25% following another month of growth in household spending and business investment along with slowly improving employment data. Wells is a net beneficiary of increased interest rates. As rule of thumb, for 1% increase in rates, net interest margin would improve by 5-15 basis points in 12mths, and net interest income would rise by 2%-5% in the first year.

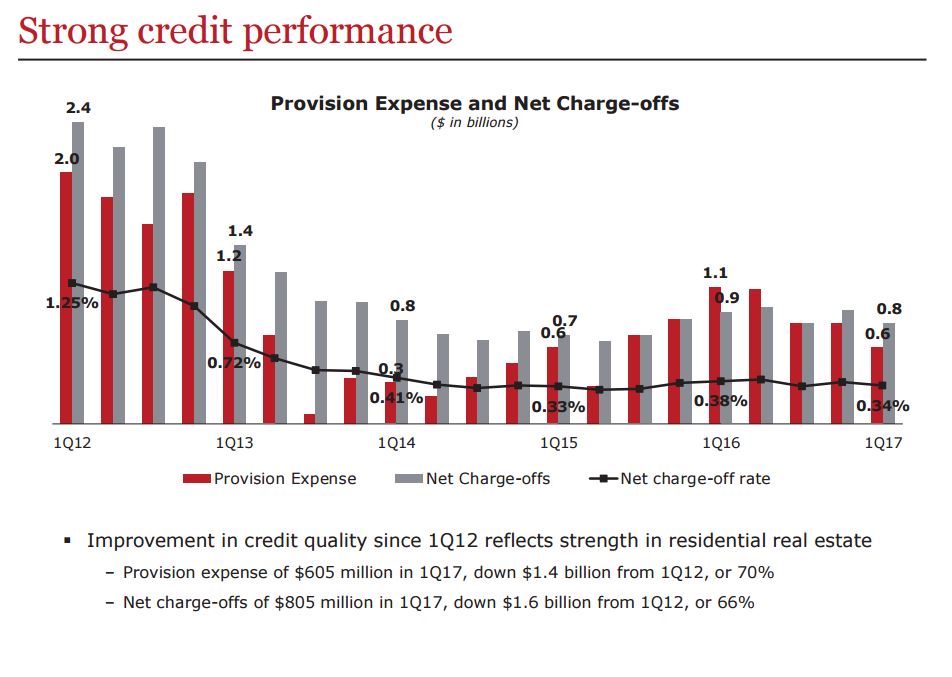

Strong 1Q17 results reflect the strength of Wells diversified business model. 1Q17 was the 18th consecutive quarter of generating earnings greater than $5 billion. Industry leading returns with 1Q17 Return on Assets (ROA) and Return on Equity (ROE) of 1.15% and 11.54%, respectively.

Risks

Banks and Wells in particular are closely linked to US economic cycle. Banks suffer from asymmetric pay-off, with limited upside (at best hope to have the loans repaid) during good times and unlimited downside (credit default) during bad times. Therefore, high unemployment, low economic growth, a lack of demand for credit, and an unfavorable interest rate environment are all impactful risks for Wells.

Wells is facing digital competition from emerging digital payment platforms, peer-to-peer lending players, and robo-advisory services in investment management. Wells will need to adapt to the new technologies and meet customers increasing expectations of convenience and low cost in managing their money.

Durable long-term advantages

- Diversified and balanced revenue sources

- Industry leading distribution

- Leading market share in key financial products

- Large and low-cost deposit base

- Relationship focus

- Credit risk discipline

- Capital strength

Valuation

Fair value estimates depend largely on long-term yield curve expectations. Wells expects to operate at the low end of its ROA and ROE targets of 1.10-1.40% and 11%-14%, respectively. Net interest income is expected to grow by low-to-mid-single percentage points in 2017. 2017 efficiency ratio expected to be 60-61%, above the 55-59% target set out in last year’s investor day. Net payout ratio target of 55-75% remains unchanged.

Consistent with ROE range of 11% – 14%, Wells is worth between 1.2-1.5 multiple of equity. Book value per share at $35.70 per share thus translates to fair value estimate of between $43.00 – $54.00 per share. Applying margin of safety of 20%, investors may wish to start adding at prices between $34.40 and $43.20.

Bulls Say

- Wells has unparalleled access to low cost deposit base and lasting relationships with many households and SME businesses that are difficult to replicate.

- As the interest rates environment normalizes, Wells balance sheet is able to reprice the loans and put additional capital to work at attractive rates, thus driving interest income and the associated non-interest fees.

- Emerging technology platforms do not wish to replace banks’ balance sheets and prefer to operate in asset light model. Banks such as Wells on the other hand have the ability to deploy technology to automate, improve user experience, lower the cost and deploy IA technologies to improve lending decision making.

Bears Say

- Customers are deserting banks in favor of online products. Traditional banks will become utilities providing capital but value will transition to online platforms.

- Low interest rates will persist for decade or more. Furthermore, Well’s bonus account opening scandal will result in much stricter rules on selling and Wells will therefore not be able to aggressively cross-sell financial products and grow its non-interest income, a key source of competitive advantage.

| No. | Owner's checklist criteria | Assessment | Comments |

|---|---|---|---|

| 1. | Is the business simple and understandable? | Yes | Wells business is centered on collecting low cost deposits and lending them out at interest rate margin, whilst at the same time manage prudently the credit risks of lending and cross sell other financial products to increase non-financial income. Banks earn their profits with balance sheet (not equity), and Wells balance is positioned very well to withstand a range of economic scenarios. |

| 2. | Does the business have a consistent operating history? | Yes | Wells has some of the longest and most consistent track record in the banking industry, globally. |

| 3. | Does the business have a favorable long term prospect? | Yes | Wells’ successful model, we believe, is well positioned to thrive in the future, as Wells digitizes its operations, allows customers to manage money more conveniently and deploys much needed technology to remain competitive in the face of emerging competition in digital payments, peer-to-peer lending, and robo-advisory investment management services. |

| 4. | Is management rational in capital allocation decisions? | Yes | Net payout ratio target of 55-75% remains unchanged. Wells eschews acquistions on non-core areas (such as investment banking) and focuses its banking activities primarily in the US. |

| 5. | Is management candid with its shareholders? | Yes | Yes, management has been mostly candid in assessing it's problems and the necessary solutions as evidenced by management resolute response fraudulent bank account openings. |

| 6. | Does management resist the institutional imperative? | Yes | Yes - management is very disciplined in focusing Wells capital, attention and efforts on its core business, including managing its loan book prudently and avoiding loose lending standards. |

| 7. | Focus on Return on Equity not Earnings per share | Yes | Wells expects to operate at the low end of its ROA and ROE targets of 1.10-1.40% and 11%-14%, respectively. Net interest income is expected to grow by low-to-mid-single percentage points in 2017. 2017 efficiency ratio expected to be 60-61%, above the 55-59% target set out in last year’s investor day. |

| 8. | Calculates "owner earnings" | Yes | Wells generates heathy levels of capital and has been allowed by FED to resume dividend and share repurchases. The payout remains consistent at 55%-75% of net earnings. |

| 9. | Looks for companies with high profit margins | Yes | Wells expects to operate at the low end of its ROA and ROE targets of 1.10-1.40% and 11%-14%, |

| 10. | For every dollar retained, create at least one dollar of the market value | Yes | Yes, management has increased value of the franchise with smart M&A (Wachovia, GE Capital) as well as shareholder friendly buy back programme. |

| 11. | What is the value of the business? | Yes | Stable & low cost deposit base, high net interest margin, high non-interest incomes, lasting customer relationships and prudent lending practices. |

| 12. | Can the business be purchased at a significant discount to its real value. (DCF) | Not yet | Consistent with ROE range of 11% - 14%, Wells is worth between 1.2-1.5 multiple of equity. Book value per share at $35.70 per share thus translates to fair value estimate of between $43.00 - $54.00 per share. Applying margin of safety of 20%, investors may wish to start adding at prices between $34.40 and $43.20. |

{kind=link}

0 Comments