Facebook suffered 20% crash following Q2’18 disappointing revenue and expense guidance. Management has flagged slower growth and higher cost owing to actions taken to address privacy concerns, GDPR legislation, and ongoing investments in the platform.

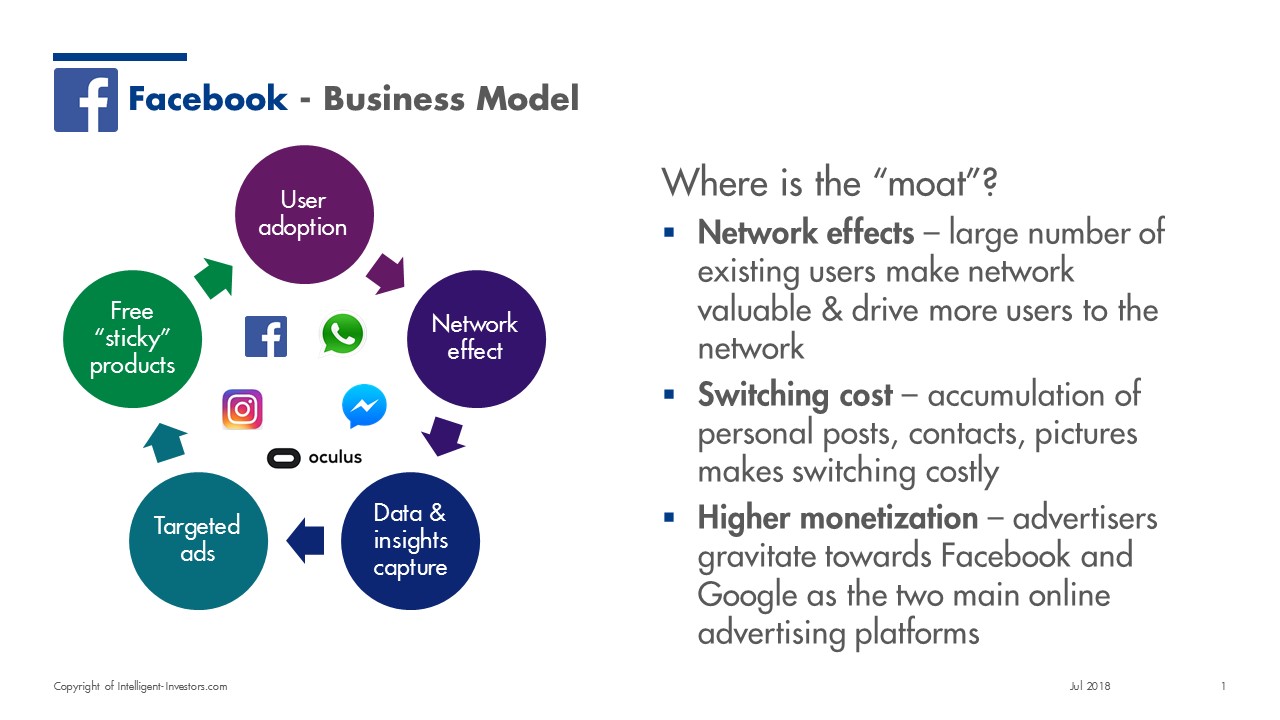

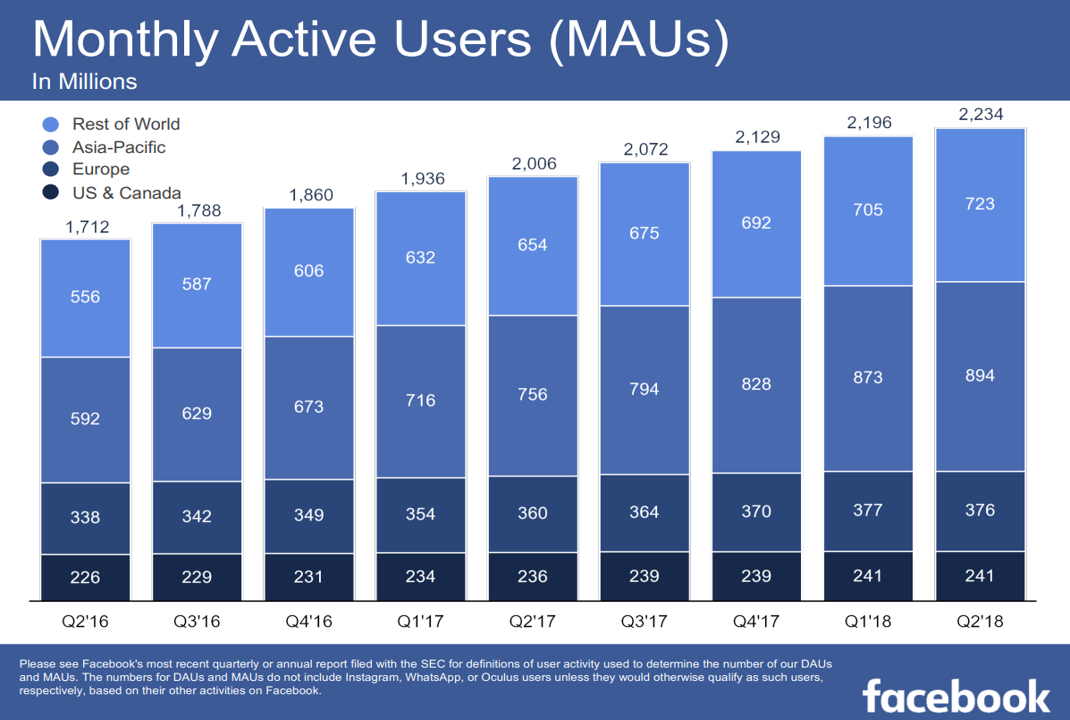

- Facebook is still the largest social network in the world with over 2.2bln monthly average active users engaging in one of Facebook’s services (Facebook, Instagram, Messenger, Whatsapp)

- Sticky business model with free “addictive” services driving user adoption, network effect, profiling data collection and targeted ads

- Together with Google, Facebook commands an effective duopoly in the online advertising market with a 20% market share

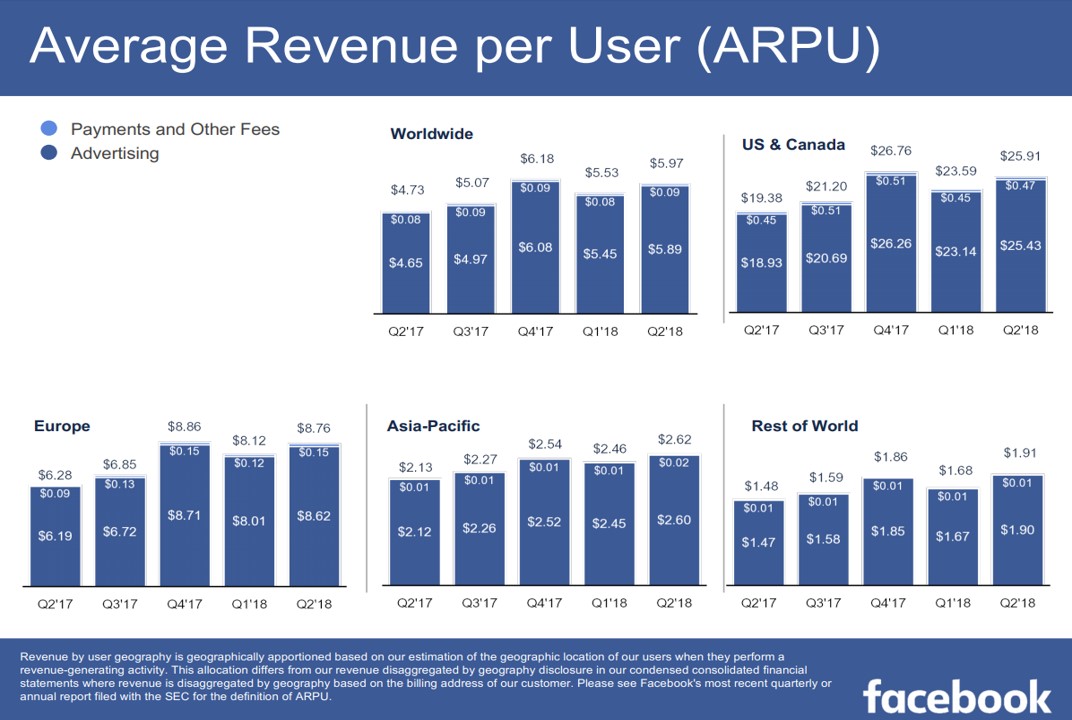

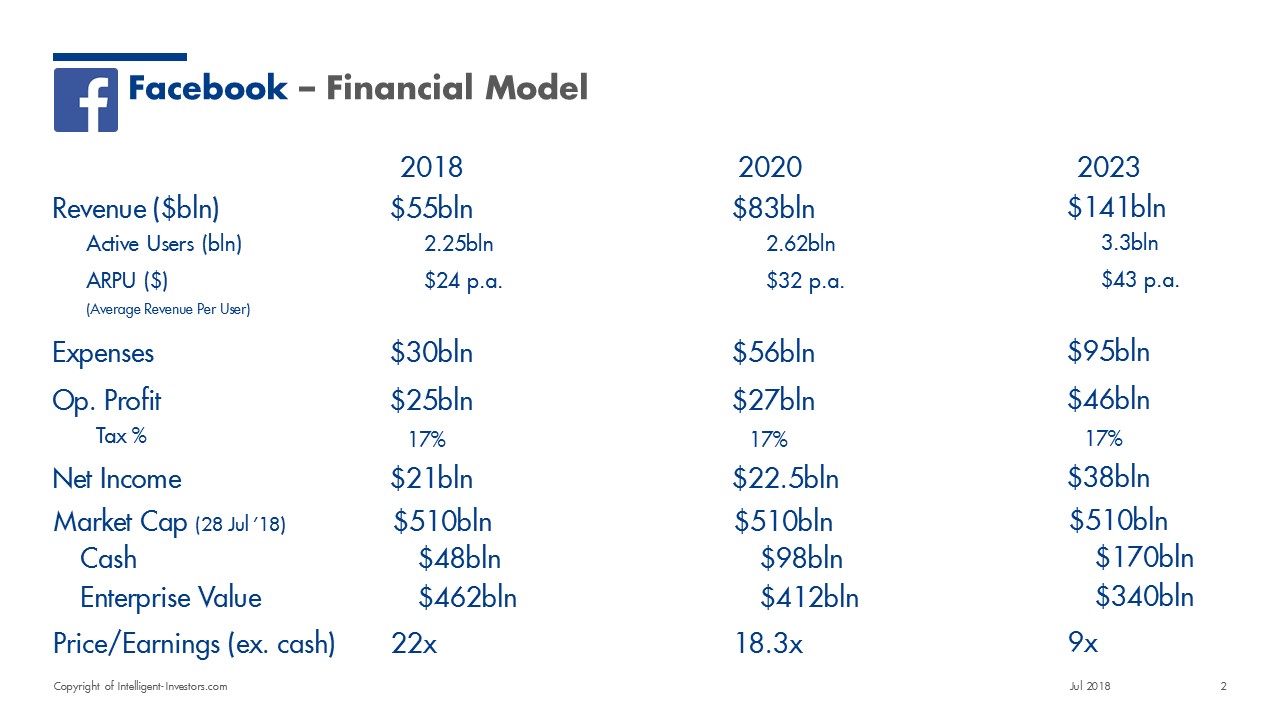

- With 2.2bln average monthly users and $25 as an average annual revenue per user, Facebook has head-room to grow revenues further. There is a market opportunity the size of existing Facebook still left

- The company is highly cash-generative with $48bln of cash on the balance sheet, and set to grow further

- Expenses are growing fast as the company invests in the platform, safeguards, GDPR privacy law compliance, and new growth options (e.g. TV service)

The company has suffered 20% share price fall after warning of slower growth and ongoing expense increases.

Management has offered a long-term operating margin outlook of 35% vs current >40% and revenue growth slowdown to high single digits.

Facebook has a number of new products with additional monetization potential.

| Durable Competitive Advantage | Narrow |

|---|---|

| Range of Fair Value Estimate | $150.00 - $220.00 |

| Stock Price | 174.89 |

| Consider Buying Below | $150 |

| 52 Wk range | 218.62 - 149.02 |

| Market Cap. | $512bln |

| Volatily | High |

| Balance Sheet | |

| Shareholder Equity | $77.6bn |

| Adjusted ROE (%) | 26.6 |

| Net Debt (Cash) | $44bln (net cash) |

| Debt/EBITDA | n/a |

| Potential Appreciation | -15% +30% |

| Dividend Yield (%) | 0.0% |

| PE Data | |

| 2017 | 28.6 |

| 2018 | 24.1 |

| 2019 | 21.7 |

| 2020 | 18.3 |

Increasing CAPEX investment eating into free cash flows – This year marks a ramp-up in capex from $6.7bn to $15bn, or 26.4% of sales.

User disengagement from Facebook platforms – late millennials/early generation Z are less prone to use Facebook. US Generation Z users appear to have declined by 10% last year, and late Millennials by 5%.

Competing social platforms (Snap) and ongoing inability to access Chinese markets will limit the user adoption and monetization potential.

Adverising spend shifting to other platforms (e.g. Google, Amazon, Microsoft) and/or weakening economy would severely limit Facebook’s ad growth.

Lack of diverse income channels with 99% of revenue still derived from the ads.

Increase government scrutiny, onerous legislation or self-initiated measures may limit usage, further adoption and monetization potential.

long-term BUSINESS QUESTIONS & DYNAMICS

- Q: Will Facebook Maintain its preeminence in the social networking segment? A: We believe so, although predicting user behavior is a fickle business.

- Q: Will user continue to engage with the platform? A: Yes, humans are social animals and Facebook has tapped into a deep and lasting need for people to share, connect, and socialize.

- Q: How well will Facebook be able to monetize ongoing usage? A: Users don’t pay for the services, advertisers do. We believe that as long as users remain engaged with Facebook, advertising dollars will follow.

- Q: Will competitors or government inflict a lasting damage to the Facebook business model? A: Facebook will need to invest to keeping the platform healthy and sustainable. Competitors will struggle to replicate network effects and compel users to switch easily.

On the price-to-earnings basis, Facebook isn’t cheap but also not expensive – 2019 PE of over 20, falling to 18 in 2020 and below 9 by 2023. on EV/EBIT, valuation is comparable to other S&P stocks also thanks to higher levels of growth and significant cash balances with no debt.

The margin is safety is arguably thin and further share price decrease would help to make the investment case clearer. Facebook arguably has a robust business model and proven track record of monetizing its user base.

Whilst below calculation is a good base case scenario, we could envisage much more adverse outcomes with flattening growth and PE compression with a further 30% downside from here. At the same time, we can also envision a much more favorable scenario with 30% upside.

Bottom line is that Facebook at $500bln valuation isn’t a Fat Pitch yet, would patience investors should wait for the cheaper point of entry closer to $400bln mark.

Bulls Say

- Largest social network with the most users spending a lot time, Facebook offers advertisers valuable targeted avenues to reach broad audience

- Average revenue per user is still very modest at $25 per user per year, with further room to grow, given the time and depth of engagement that users have with the platform

- As interest penetration increases, Facebook app is often one of the first that users interact. User growth provide Facebook with sizeable addressable market.

Bears Say

- Facebook is very reliant on ads for revenue with no alternative revenue streams

- Governments may impose regulations that limit the collection of user data adversely impacting ads potential

- Competing platforms (Snap) or alternative use cases (Search through Google, shopping on Amazon) will redirect ads dollaers away from Facebook

{kind=link}