Investment Thesis

U.S. Bancorp (USB) is the fifth-largest commercial bank in the United States, with $460 billion in assets. The company operates 3,045 banking offices and 4,725 ATMs and provides a comprehensive line of banking, investment, mortgage, trust, and payment services products to consumers, businesses, and institutions.

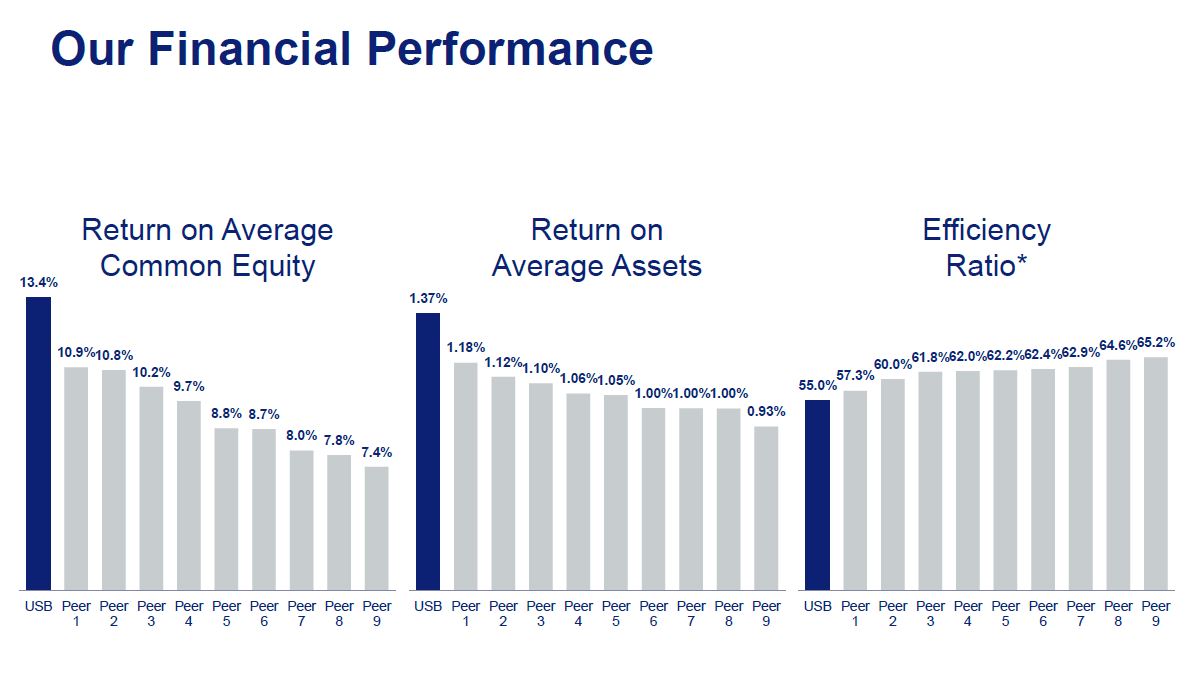

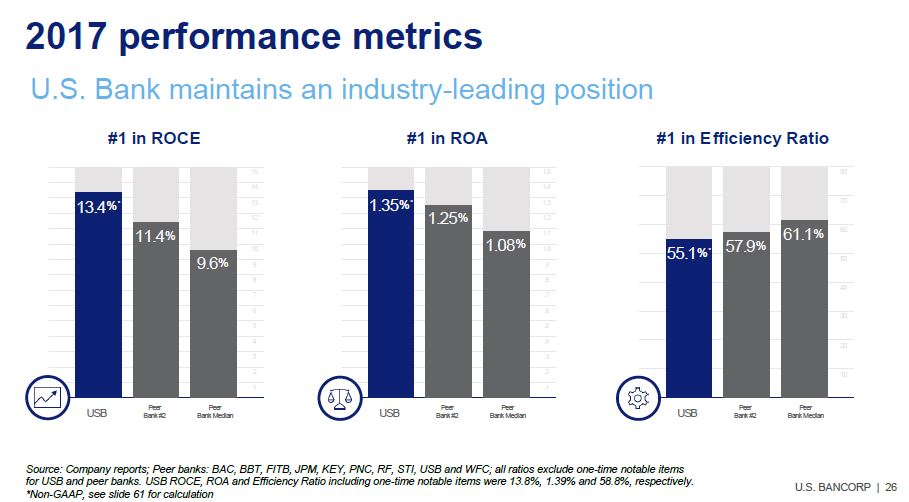

US Bancorp has a leading banking franchise with top of the range Return on Equity 15%, Return on Assets of 1.4%, Efficiency ratio of 55%, and strong asset quality with Net Charge-offs of 0.5% annually.

Assessment of the present franchise

The business franchise is characterized by a balanced mix of revenue streams and the simplicity of the balance sheet. In addition to strong consumer and wholesale banking with attractive net interest margin, US Bancorp has a leading franchise in Payments, Wealth-management, and Trust services which provide fee-based revenues. The balance sheet is funded by $340bln of low-cost deposits with an average cost of 0.5% annually. On the asset side of the balance sheet, US Corp holds a well diversified and conservatively underwritten loan book comprising $280 billion of loans and $115 billion of investment assets (mainly comprising US Treasuries and US government agency backed securities).

US Bancorp is arguably one of the best-managed banks in the U.S., as evidenced by a long track record of strong profitability, strong credit culture and underwriting discipline, and management’s attention on treating shareholders’ capital fairly.

| Durable Competitive Advantage | Wide |

|---|---|

| Range of Fair Value Estimate | $50 - $65 |

| Stock Price | 54.14 |

| Consider Buying Below | $50.00 |

| 52 Wk range | 58.50- 48.49 |

| Market Cap. | $88.5bln |

| Volatily | Medium |

| Balance Sheet | |

| Shareholder Equity | $44bn |

| Adjusted ROE (%) | 15.3% |

| LT Debt | $37.1bln |

| Debt/EBITDA | N/A |

| Potential Appreciation | -10% +20% |

| Dividend Yield (%) | 2.2% |

| PE Data | |

| 2017 | 18 |

| 2018 | 13.3 |

| 2019 | 12.4 |

| 2020 | 11.4 |

Permanence of US Bancorp’s franchise

The cornerstone of a profitable banking franchise remains low cost and stable deposit base, which US Bancorp is able to intermediate at an attractive Net Interest Margin, presently exceeding 3% annually. The core retail and wholesale banking is 60% of US Bancorp revenue. The world hasn’t yet invented a better way to intermediate money and the lending part of the franchise, therefore, appears to have a durable moat for many years out, in our opinion. Investors often hear about fin-tech and other technology companies disrupting banking model, however the basic model of banking which entails taking deposits and making loans remains well protected by banking regulations, the need for low-cost deposit base, and a large balance sheet.

Arguably the “moat” for payments business, responsible for 30% of revenues, is narrow as non-banking entities have been innovating in this space as a way to strengthen their hold on existing customers. Major players include the likes of Apple Pay, Android Pay, PayPal, Square, and Zelle. US Bancorp payments business accounts for 18% of the income and services other banks, corporates, and merchants. Its payments business model is highly scalable with almost zero incremental cost and capital requirement for processing additional transactions after initial fixed investment in the platform.

Finally, trust services, responsible for 7% of revenues, is a very mature and “moaty” business as the market share is concentrated in the hands of a very few players and the threat of new entrants is low.

US Bancorp’s primary competitive advantage seems to stem from it’s very low cost deposit base, efficient cost structure, large scale, high switching cost for its clients, and disciplined underwriting.

Of the three franchises described, the moat in the retail and wholesale banking and trust services appear to have some permanence looking 5 or 10 years out, however payment services is subject to a more intense competition.

Room for future growth

The bank is currently present in 25 states with further room to grow. The bank benefits from super-regional scale as well as from several national businesses (such as credit cards and mortgages). This presents an opportunity to gather deposits and capture market share from both pre-existing customers as well as new client relationships.

Historically, the bank has growth through branch acquisition which would enable it to capture the deposit base, however increasingly the customer relationship acquisition has shifted to the payments platform, with other higher value services attached at the later stage.

Payment digitization is reaching corporate clients. The management has stated that half of business-to-business payments are still executed by check and this creates an opportunity to convert corporate clients to electronic payment platform. US Bancorp has also tested a small business digital lending platform that can provide a credit decision in less than a minute versus current 2 week lead time.

US Bancorp’s management believes that banking industry is entering a period of consolidation as smaller banks struggle to match the fixed cost investments in technology and digital solutions that require a scale to be profitable. US Bancorp currently operates on one integrated back-office system which helps to reduce cost of running multiple legacy systems.Management is also investing heavily in digital solutions to compete with the biggest national banks.

Management track record

The fact that Berkshire Hathaway is major shareholder helps to reassure us that US Bancorp’s management will continue to act rationally and in the best interest of shareholders.

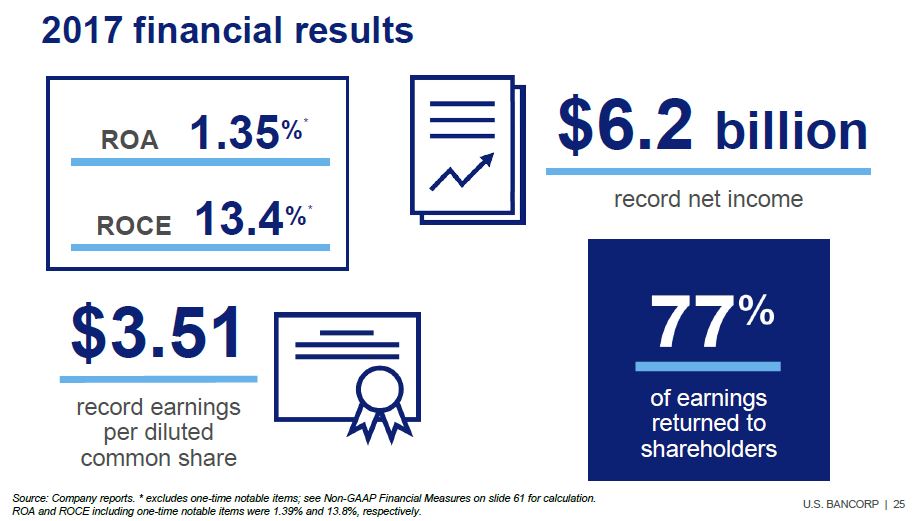

Besides that point, US Bancorp has a long history of rational and top-class management that acts in the best interests of shareholders and stewards shareholders capital wisely. Even during 2008/09 crisis US Bancorp didn’t post a loss-making quarter. Over the past 20 years US Bancorp has delivered 400% total shareholder return, increased market share in the markets it competes in, maintained leading levels of profitability and efficiency. Management’s track record arguably speaks volumes about the company’s ability to deliver consistently attractive returns.

Managements has reiterated its commitment to lending discipline, rational capital allocation, and the technology innovation to maintain relevance to the customer. On the subject to technology investments, management is confident that the bank can compete against the largest players though it also recognizes the structural shift of banking services towards digital solutions and ways of interacting with the customers. US Bancorp intends to spend $1.2 billion on technology investments on top an existing $1.5 billion of operating cost to maintain its technology.

The company is under an agreement with regulators to strengthen its anti-money laundering and bank secrecy act compliance processes, with management indicating that company has completed the pre-work required and is awaiting regulators to lift the agreement.

Risks

Risk factors

U.S. Bancorp is not large enough to be considered a global systemically important bank and is, therefore, able to avoid additional capital requirements. The bank is subject to the Federal Reserve’s annual stress tests and liquidity requirements because it has more than $250 billion in assets.

The banking industry is undergoing a structural shift towards digital solutions. Although we’re seeking the potential for some margin compression, we’re somewhat more sanguine about the prospects of existing banks due to the following reasons:

1. Banks have a large scale and offer a more complete one-stop-shop product offering to stay relevant and meet the needs of a range of clients

2. Banks have the ability to largely replicate many of the new offerings such as mobile and payments solutions

3. Banks benefit from their regulatory status including a federal deposit insurance and an access to the nation’s payment system infrastructure.

As with any other banking institution, US Bancorp carries a small but non-zero systemic risk due to the inherent volatility of financial markets and credit cycles.

long-term BUSINESS QUESTIONS

- Question: Will US Bancorp maintain its strong franchise in the banking, payments and trust businesses?

- Answer: We believe the answer is yes, the world hasn’t yet invented a better deposit and lending model than a bank and US Bancorp has a strong banking franchise with the low-cost deposit base. Payments arguably will be an area of future innovation and more intense competition, US Bancorp has as a good chance as any other player to succeed, playing from the position of strength. Trust business appears “moaty”.

- Question: Will US Bancorp manage through the next credit crisis and credit cycle?

- Answer: US Bancorp has not posted a loss-making quarter even in the depth of the crisis. Management’s track record in prudent lending practices and shareholder value creation makes us believe that US Bancorp is well-positioned to weather a deterioration in the credit cycle.

- Question: Will management change its attitude to the risk profile?

- Answer: Management has reiterated its view that disciplined underwriting will take precedent over loan book and market share expansion.

Valuation

There are many variables that go into the valuation of the financial institutions. Great many banks are in fact near impossible to reliably value due to their opaque and complex balance sheet. Assets may or may not turn out to be valued at 100 cents of market value on every dollar reported, yet liabilities are always worth at least 100 cents on dollar reported. US Bancorp is one of the few simple, yet profitable bank franchises, that lend themselves to a valuation estimate using reasonable and rational set of assumptions.

It should be noted that with banks, investors should place a great deal of importance on the historical track record as an indication of future permanence and durability of the banking franchise, rather than get persuaded by the current low book or earnings multiple where the historical track record isn’t convincing.

We’ll examine both book-value and earnings value.

Book value approach

Book value or net asset value measures how much capital the bank has accumulated. US Bancorp has a net book value per common stock of $28, of which $5 is in intangible goodwill, giving $22 of tangible book value. This is a measure of how much productive capital shareholders have invested in the company including accumulated profit.

US Bancorp earns about 19% return on tangible equity (and 15% return on equity), which is an excellent rate of return for a financial institution. Per management’s guidance, the company plans to pay out between 60-80% of its earnings and re-invest the rest at 15-19% return on incremental capital. We anticipate the tangible book value to grow accordingly and model the book value movements in the table below.

- 2018: $28.03

- 2019: $29.93

- 2020: $32.15

- 2021: $34.50

- 2022: $37.03

- 2023: $39.74

The appropriate price to book value ratio to apply ranges from 1.7 to 2.3 depending on assumed return on incremental capital and payout ratio. Assuming 17% return on incremental capital and 80% earnings payout, we derive Price-to-book multiple of 2. Over the past twenty years, US Bancorp traded at year-end book value mutliples ranging from 1.6 to 3. Our multiple of 2 is reasonable.

This gives the estimated market value of $56 a year for year-end 2018.

Earnings value valuation

Using earnings method, we project the components of the total return that the stock is reasonably likely to provide over 5- to 10-year time horizon, based on the conviction in the permanence in the current franchise profitability that far out.

US Bancorp is projected to earn some $4.40 dollars share next year, of which it has paid out about 80% of the earnings or $3.50 dollar per share in form of dividends and share buy-backs. The remaining 20% get reinvested at between 15-19% depending on what we believe the company can earn on the incremental capital.

$3.2 dollar per share in dividends and repurchases is worth about 6.5% yield to the investor at the current stock price of $54.

Remaining $0.88 dollar per share get reinvested at 15-19% return so every dollar invested creates between $1.5 dollar to $2 dollars of additional value over time. US Bancorp is already a large institution and there are not as many new investment opportunities, hence the company retains only between 20-30% of the earnings and we prefer to assume the lower end of that range. Of the $0.88 dollar of retained earnings per share, we estimate the company is creating an additional $1.5 dollar of value, which translates to an additional 2.7% return for the shareholder.

Additionally, US Bancorp benefits from payments and trust businesses which don’t require much capital and will grow in line with the GDP. Trusts and payments account for about one-third of the earnings and moderate growth of 3% for these businesses translates to about 1% uplift to the whole company and thus the 1% additional yield to the stockholder.

The total prospective return for the stockholder is thus about 10%, made of 6.5% return in dividends and share buybacks, 2.7% return from earnings reinvestment, and 1% return from an asset-light business growth.

20-Year Track Record

For the record, US Bancorp has achieved total shareholder return of 600% over the past 20 years. The details are included in the table below.

| 20-Year Total Shareholder Return | ||||

| Dividend Reinvestment Options | ||||

| Reinvestment in Security | Risk Free Reinvestment | |||

| Total Dividends ($) | 21.02 | Total Dividends ($) | 16.42 | |

| Shares Purchased | 0.66 | Annualized Reinvestment Rate (%) | 2.099 | |

| Total Shares Owned | 1.66 | Reinvestment Income ($) | 3.11 | |

| Capital Gain/Loss ($) | 53.94 | Capital Gain/Loss ($) | 39.26 | |

| Total Gain/Loss ($) | 74.96 | Total Gain/Loss ($) | 58.8 | |

| Total Return (%) | 504.93 | Total Return (%) | 396.08 | |

Bulls Say

- Strong fee revenue from payments and trusts businesses helps to counter-balance the lending side of the business

- Strong balance sheet, good economic growth, rising interest rates and easing of regulatory pressures help to create a more profitable investment climate for the banks

- US Bancorp benefits from low-cost deposit base, lean operating model, investment in technology solutions, and continued underwriting discipline.

Bears Say

- Deterioration in credits will hurt profitability as provisions for bad loans is sure to increase from the present historically low base.

- Intense competition in the payments space is slowing growth and compressing margins.

- The long-term banking business model will be challenged with fin-tech innovation across elements of the banking value chain.

For those who want to find out more about US Bancorp, below is the link to the company’s 20-year financial statements summary. We place a great deal of importance on historic track record.

{kind=link}