The Company

Petrofac remains a leading engineering and construction contractor for Oil & Gas operators. Petrofac portfolio centers on large-scale investments in oil and gas infrastructure EPC projects in competitive areas such as Middle East. Petrofac has historically maintained good relationships with National Oil Companies, NOC’s which hold majority of low cost resource base.

The Issue

Petrofac was hit by UK’s Serious Fraud Office (SFO) investigation into alleged bribery, corruption and money laundering related to the SFO’s investigation of Unaoil. SFO has branded Petrofac as non-cooperative by SFO and rejected the findings of Petrofac’s internal investigation in the allegations.Unaoil, Monaco based firm, is alleged in media reports to have been used by numerous multinational companies as a conduit to make illegal payments to secure work in Kazakhstan. In August 2016, Petrofac announced that its own independent

investigation found no evidence confirming the payment of bribes. Petrofac confirmed that it engaged Unaoil for the provision of local consultancy services primarily in Kazakhstan between 2002 and 2009 and published findings of its investigation in 2016 annual report. Investigation was completed by Freshfields with support from KPMG.

Latest Developments

Petrofac board announced suspension of COO and board is signaling higher level of cooperation with SFO. CEO remains on seat, however has recused himself from the investigation, which will be handed directly by a Committee of the Board.

Market Reaction

Since news broke of the SFO investigation earlier in May, PFC has lost USD1.7bn / GBP 1.3bn of market cap, this translates to cumulative 60% share price drop in the past 2 months.

Market remains concerned that Petrofac will be facing heavy fine, management discontinuity, unability to win new business, debt default event and/or share rights issue to shore up the balance sheet. Fines could be of up to $800mln assuming worst case scenario.

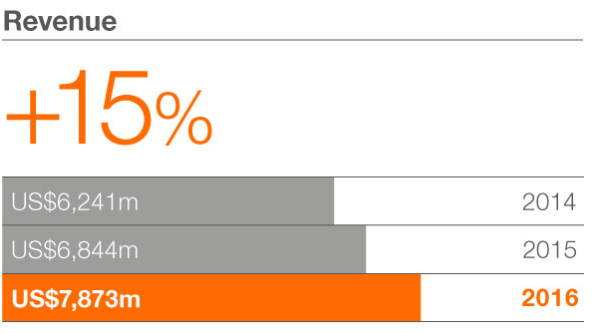

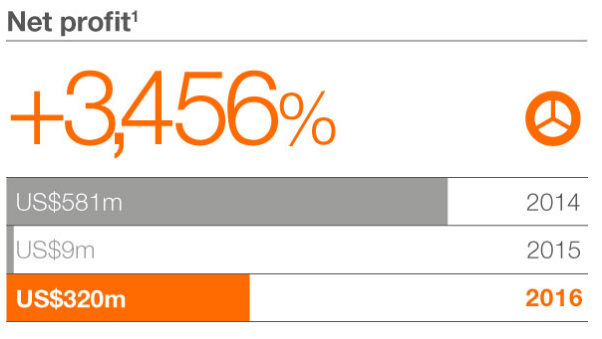

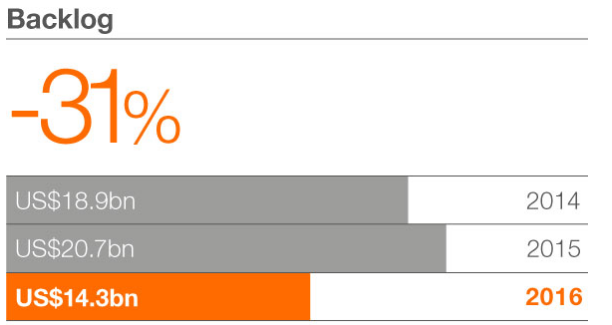

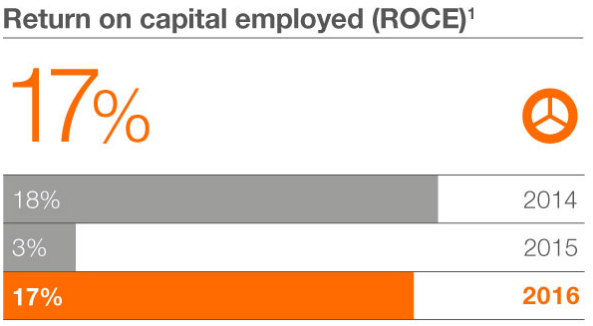

Petrofac - Company Profile

Solid track record of delivery

Credit Risk

Under the bank’s revolving credit terms, a default event could include “commencement of litigation, arbitration or other proceedings deemed to be material”, however the interpretation of such clause would require judgment applied.

Petrofac is expected to suspend dividend and focus its resourcing on strengthening the balance sheet to weather the difficult period ahead.

Petrofac’s net debt stands at $620mln, which is 2.5 years of profit, manageable in our opinion.

New Business Impact

In the short run, Petrofac management will face distraction from ongoing day-to-day management, in order to deal with the investigation, and this will likely impact Petrofac’s ability win tenders, execute existing work and continue to transform the business. The uncertainty will be also an unwelcome surprise to many of Petrofac’s customers who will will be asking questions and potentially holding back new business in order to mitigate risks.

Valuation

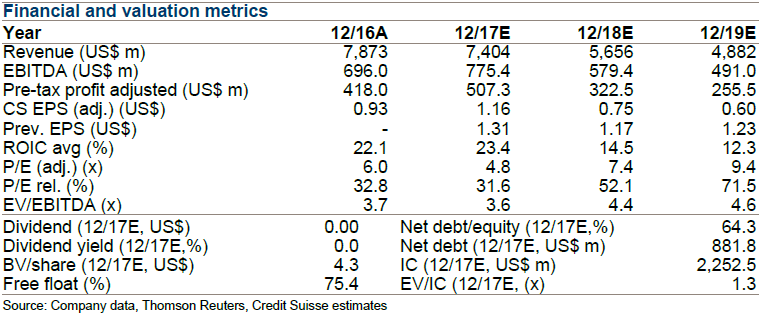

Petrofac has become the cheapest oil & gas service company in Europe with PE ratio of 5. Petrofac is trading at Price to Book ratio of 1.1 ($4.30 book value per share vs $4.80 share price).

Business has inherently good cash generating capacity, albeit volatile. In a good year, Petrofac can generate $300mln of cash flows to the firm after Capex investments. At enterprise value of circa $2,500mln, Petrofac is trading at multiple of 8.3 of free cash. This is rather attractive multiple considering historical range of multiple of 10-15.

Next Steps

SFO investigation won’t be completed anytime soon and any potential investor will have to get used to the uncertainty the business is facing. Whilst Petrofac is paying the price of reputational risk, the conclusion of investigation remains wide open. Even if Petrofac is prosecuted and found to have been acted criminally, it is reasonable to assume that company would attempt to arrive at a settlement with SFO, akin to recent Rolls Royce settlement.

It should be noted that SFO intention is:

to enable a corporate body to make a full reparation for criminal behavior without the collateral damage of a conviction (for example sanctions or reputation damage that could put the company out of business and destroy the jobs and investments of innocent people.

Business Moat

Petrofac doesn’t have business moat. It’s business is commoditized and hence low margin. However, Petrofac is well positioned to benefit from eventual upturn in the market activity with many long-standing relationships in low-cost regions in Middle East and North Africa. Furthermore, Petrofac has proven track record of delivering business competitively and on commercial terms.

The current valuation place Petrofac in a “turnaround” category. However, it should be noted that things can get worse before they get better, uncertainty is likely to persist and stock likely to underperform in the interim, and Petrofac still remains subject to volatile Oil & Gas market conditions.

Conclusion

Petrofac is an attractive turnaround bet, with expected positive pay-off but high volatility. Investors must be prepared to live with volatility, potentially more damaging news, and be prepared to suffer potential losses in the event of dilutive rights issue.

{kind=link}

0 Comments