Investment Thesis

Imperial Brand’s strategy centers of maximizing cash returns to shareholders through cost cutting, focused set of growth brands and tight capital allocation. Imperial generates leading profit margins and has embarked on the multi-year journey to reduce number of brands in its portfolio by migrating existing customers to more profitable “growth” brands.

Cash Yield – Management has a good track record in delivering cash returns to shareholders. Dividend yield is 5% and management has guided for 4-8% annual earnings growth over medium term. Cash conversion has averaged 90% over long-term. Even without any significant improvement in the current trading environment Imperial stock is trading at a discount to tobacco sector and its dividend will put a floor on the downside. 5% dividend coupled with 4% growth in earnings (bottom of the range), will deliver 9% return to a shareholder over medium term, possibly more.

Competitive Advantage

Brand portfolio – As with all tobacco companies, Imperial possesses strong portfolio of attractive tobacco brands and durable competitive advantages. By their nature, the products are high margin, highly addictive and with high brand loyalty. Imperial has historically been able to offset volume falls with price increases, given low price-elasticity of tobacco products. Outside elicit trade, tobacco companies generally behave rationally and eschew price competition – tobacco industry can indeed be labelled a rational oligopoly.

Barriers to entry – Advertising bans are creating barriers to entry for new competition. Key risks included plan packaging for tobacco companies, similar to measures enacted in Australia, and currently proposed in the UK. Equally, e-cigarette market is poised to take share over time, either in the form of vaping (Imperial has blue brand present) or “heat-but-not-burn” products where Imperial is absent (e.g. Philip Morris IQOS products). Imperial has the depth of distribution and brand portfolio to complete in these markets effectively, albeit against smaller and more aggressive competitors than is the case with existing tobacco business. We believe that as heat-but-not-burn category becomes more material, Imperial will be able to enter the market.

| Competitive Advantage | Wide |

|---|---|

| Fair Value Estimate | GBP 4,150.00p |

| Stock Price | GBP 3,440.41p |

| Consider Buying Below | GBP 3,320.00p |

| 52 Wk range | 4,154.00p - 3,324.00p |

| Market Cap. | GBP 33.1bln |

| Volatily | Medium |

| Balance Sheet | |

| Shareholder Equity | GBP 5.2bln |

| ROE (%) | 41.9% |

| Net Debt | GBP 13,8 |

| Debt/EBITDA | 3.7 |

| Potential Appreciation | 20% |

| Dividend Yield (%) | 4.9% |

| PE Data | |

| 2016 | 13.8 |

| 2017 | 12.8 |

| 2018 | 12.3 |

| 2019 | 11.7 |

10% Market Share Globally

30% Net Margin on GBP 8.6bln of Sales

4.9% Dividend Yield

Latest developments

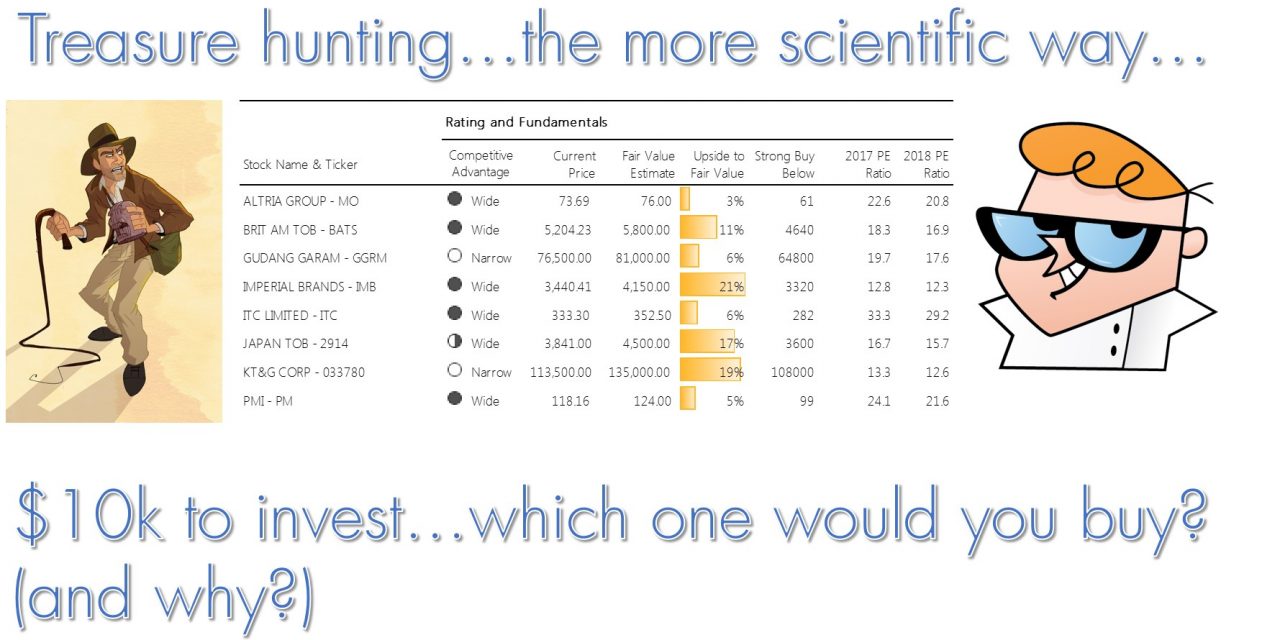

Imperial Brands is UK based 4th largest tobacco company with 10% global market share (outside China), and an extensive portfolio of tobacco products in Europe, US and Russia. Despite highly cash generative nature of its business, the stock has been falling steadily in recent months due to perceived lack of products in an emerging heated tobacco product category (e.g. Philip Morris IQOS). Company also reported in its most recent announcement that volume declines weren’t offset by price increases, has historically been the case. Stock has been hovering around 18 months low and become the cheapest tobacco stock amongst international tobacco companies. We believe that stock now offers an attractive entry point.

Risks

Declining smokers’ population – Number of smokers in developed countries is declining whilst existing smokers are trading down to cheaper brands or elicit trade. Imperial may be facing double risk of declining volumes and lower price realization. New smokers in emerging countries may not be able to fully offset declining profitability of development markets.

Expropriation of brands – Australia and now UK have enacted legislation for plain packaging. This means that Imperial, and other tobacco companies, may be unable to fully exploit the brand loyalty.

End of nicotine monopoly – Cigarettes, cigars and chewing tobacco have long had a virtual monopoly on delivery of nicotine, the addictive ingredient of cigarettes. With the advent of vaping and heat-but-not-burn tobacco products, the stranglehold of tobacco on nicotine delivery will inevitable end.

Durable long-term advantages

- Brand Portfolio and Brand Loyalty

- Low Cost, High Margin, Addictive Product

- Barriers To Entry

- Regulated Markets

Valuation

Imperial is selling at 30% discount on P/E and Cash-flow basis versus global tobacco peers. Some of the discount is justified due to lower growth profile. Given 5% existing dividend yield and 4%-8% medium term earnings growth, investors can reasonable expect to earn 9% total return on stock, potentially more, if stock gets re-rated.

Imperial has sizeable debt following acquisition of US brands. The debt is gradually getting paid down and we don’t expect to have adverse effect on Imperial’s credit rating. US market is characterized by good margins, low taxation and ability to raise prices to offset volume declines.

We believe that the downsize to Imperial stock is limited, underpinned by its generous dividend yield of 5%. Imperial also has an embedded sale put option. Should price fall below fair value significantly, other competitors will likely attempt to acquire. The prime candidate is Japan Tobacco which harbors global ambitions and has long been rumored as a potential suitor.

Bulls Say

- Cheapest valuation amongst international peers

- Highest margin in the industry

- Shareholder oriented management

- Entrenched position in attractive brand categories

- 4%-8% medium term growth of earnings

Bears Say

- Long-term volume declines

- Emerging product categories will eat into market share

- Lower growth and weaker pricing power vs peers

- Regulatory threat (plain packaging)

{kind=link}

0 Comments