Investment Thesis

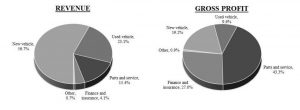

AutoNation is the largest automotive dealer in the United States, with 2016 revenue of $21.6 billion and 260 dealerships in 16 states, primarily in Sun Belt metropolitan areas. New-vehicle sales account for about 57% of revenue, however profit is primarily derived from parts and services (43%), finance and insurance (27%), new vehicle sales (20%) and used vehicle sales (10%).

Whilst new vehicle sales are highly competitive, low margin and seasonal business, AutoNation benefits from diverse revenue streams generated by used vehicle sales, parts and service business, and finance and insurance sales. The higher margin parts and service business has historically been less sensitive to macroeconomic conditions as compared to new and used vehicle sales. It should be noted that although dealerships generally intra-brand competition within the state, the franchise tend to be stick and renewed by the automakers.

Whilst new vehicle sales are highly competitive, low margin and seasonal business, AutoNation benefits from diverse revenue streams generated by used vehicle sales, parts and service business, and finance and insurance sales. The higher margin parts and service business has historically been less sensitive to macroeconomic conditions as compared to new and used vehicle sales. It should be noted that although dealerships generally intra-brand competition within the state, the franchise tend to be stick and renewed by the automakers.

Furthermore, dealerships remain very fragmented market that is gradually consolidating, allowing large companies such as AutoNation to profitably acquire other dealerships and extract synergies as revenues per dealership increase over time. AutoNation has a long runway left in terms of tuck-in acquisition. Even though it is the largest new car dealership network, its market share was only 1.92% in 2016.

As cars are becoming technologically more complex, manufacturer licensed and larger scale dealerships have advantage in being able to invest in the servicing equipment and personnel training required to provide the level of service to modern vehicles.

AutoNation has 260 dealership turning over $21bln, equating to $83mln sales per dealership. Of this total, $12.2bln or 337k units were new vehicle sales, equating to $47mln or 1,300 units of new vehicle sales per store. This compares to nationwide average of 1,000 units per store.

Dealerships generally require minimal capital as vehicle inventory is generally funded by the manufacturer at very competitive rates (1% interest) so business requires minimal capital and generates heathy amounts of cash. ROE is 16% even as net margins are under 2% indicating very high inventory turnover and cheap inventory financing.

Crucially, AutoNation’s capital allocation strategy is focused on maximizing stockholder returns. As stated in the annual report AutoNation “…invest(s) capital in our business to maintain and upgrade our existing facilities and to build new facilities for existing franchises, as well as for other strategic and technology initiatives, including the next phase of our brand extension strategy … We also deploy capital opportunistically to repurchase our common stock and/or debt or to complete dealership acquisitions and/or build facilities for newly awarded franchises. Our capital allocation decisions are based on factors such as the expected rate of return on our investment, the market price of our common stock versus our view of its intrinsic value, the market price of our debt, the potential impact on our capital structure, our ability to complete dealership acquisitions that meet our market and vehicle brand criteria and return on investment threshold, and limitations set forth in our debt agreements.”

We suspect that this explicit shareholder oriented philosophy is a direct outcome of Cascade Investments 18% ownership of AutoNation. Cascade is an investment vehicle of Bill Gates and his foundation. Michael Larson, Cascade’s Chief Investment Officer, is a lead independent director of AutoNation.

Company has been repurchasing some $400mln shares annually or circa 10% of its market capitalization, a policy that we expect to remain in place at current valuations.

| Competitive Advantage | Narrow |

|---|---|

| Fair Value Estimate | $48 |

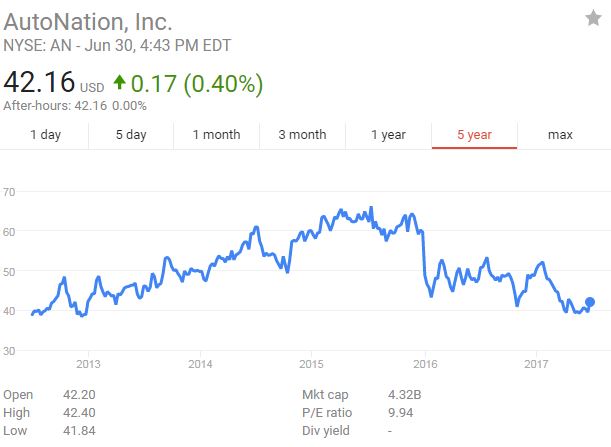

| Stock Price | $42.16 |

| Consider Buying Below | $40 |

| 52 Wk range | $54.15 - $38.20 |

| Market Cap. | $4.27bln |

| Volatily | High |

| Balance Sheet | |

| Shareholder Equity | $2.4bn |

| ROE (%) | 19.1 |

| Net Debt | $2.6bln |

| Debt/EBITDA | 3.9 |

| Potential Appreciation | 14% |

| Dividend Yield (%) | 0% |

| PE Data | |

| 2016 | 11.7 |

| 2017 | 10.8 |

| 2018 | 10.1 |

| 2019 | 9.6 |

260 Stores Nationwide

$83mln Sales Per Store

377k Vehicles Sold & 1.92% Market Share

Latest developments

Sales channels are indicating a mid-to-high 16MM SAAR (seasonally adjusted annual rate) figure for the June (vs. 16.8MM last year and 16.6MM last month). A sub17MM figure in June would mark the fourth consecutive month in the 16MM SAAR range (last time the industry reported four consecutive months in the 16MM range was in late 2014). We believe OEMs (original equipment manufacturers) will escalate incentive spending to maintain volumes and protect market share.

Valuations for dealerships have fallen as investors believe that auto sales have hit the peak of the cycle and are poised to drop from these levels. We have no special insights as to the likely auto sales levels. Low interest environment and low gas prices are helping consumers to buy new vehicle at low financing and running cost. We suspect that as interest rates normalize and oil prices increase, these will act as head-winds going forward. However, this is hard to predict and we claim no special insight.

Risks

- Short term sales are driven by economic conditions which are hard to predict and may deteriorate.

- Company may be benefiting from peak cycle earnings are number of vehicle sales have been very strong over the past few years

- Bankruptcy of a major manufacturer, withdrawal of vehicle floor plan (inventory financing arrangement), economic downturn, interest increase and oil price volatility may hurt sales, financing and insurance profits as customer postpone new car purchase.

- Long term disruption may include self-driving cars, decreased ownership as people use transfer as a service rather than purchase their own vehicle (sharing economy), emergence of new business model such as Tesla’s direct to consumer sales model, as well as emergency of internet as the primary sales channel, diminishing the value of franchises and store locations

Competitive advantages

- Largest new vehicle dealership network

- Economies of scale, synergies, investment in internet channels

- Diversifying into servicing and parts

- Territories with franchise agreements

- Vehicle floorplan financing provided by manufacturers at low rates

- Opportunity for tuck-in acquisitions in consolidating market

- Increase sales per store

- Stickiness of new vehicle customers for services and parts

- Increasing complexity of vehicles, requiring investment in equipment and training, which is more affordable to large players

Valuation

We use a DCF-based model to value AutoNation. We estimated fair value at $48 per share. Below is the full DCF model. Key DCF assumptions are terminal growth of 2.5%, terminal net margin of 2% (vs current levels of 2%), capex of 1.1% of sales (consistent with 2016 levels), and a WACC of 8.44%. We also note that we consider floorplan debt and interest as operational (i.e. we exclude floorplan debt from overall debt and correspondingly include floorplan interest.

Bulls Say

- AutoNation is the largest car dealership chain with size, economies of scale, strong operating margins and large infrastructure investment in internet sales channel, giving it advantage over smaller players in an increasingly consolidating market

- AutoNation has been rebalancing its revenue streams towards servicing and spare parts which are both higher margin and less susceptible to economic cycles.

- Shareholder friendly and opportunistic capital allocation enables shareholders to benefit from share repurchases at attractive discounts to intrinsic value, thus creating shareholder value. Similarly, opportunistic purchases of franchises allow AutoNation to earn attractive returns on its capital.

Bears Say

- AutoNation is exposure to economic cycle with wild swings in the number of new vehicles sold

- AutoNation is facing structural risks with the emergence of internet only players, fierce competitors (such as Berkshire Automotive) and direct to consumers model (Tesla)

- Long-term shift to rental model and secular drop in auto ownership and sales will hurt new car sales. Electric vehicles required minimum services as number of moving parts is much fewer than petrol/diesel engine cars.

Sales of news cars is lower margin compared to used car sales (such as CarMax model)

| No. | Owner's checklist criteria | Assessment | Comments |

|---|---|---|---|

| 1. | Is the business simple and understandable? | Yes | AutoNation business is understandable - growing dealership network granted thru franchise to sell new car, provide financing/insurance and take comission, provide servicing and parts and sell used cars obtained via customer trade-ins. Grow the dealership network by opportunistically consolidating other dealerships and/or repurchase shares depending on rates of return expectations and intrinsic estimate of the company's worth |

| 2. | Does the business have a consistent operating history? | No | Business is highly cyclical. Company has generated profits except during periods of recession when sales of new vehicles dropped significantly and company suffered a loss |

| 3. | Does the business have a favorable long term prospect? | Likely Yes | Likely yes, dealerships are consolidating favouring larger players such as AutoNation. Vehicles are getting more technically complex, requiring investments in servicing equipment and training, which is more affordable for larger dealerships. |

| 4. | Is management rational in capital allocation decisions? | Yes | Likely yes, dealerships are consolidating favouring larger players such as AutoNation. Vehicles are getting more technically complex, requiring investments in servicing equipment and training, which is more affordable for larger dealerships. |

| 5. | Is management candid with its shareholders? | Yes | Yes, management has been candid in their quarterly calls around challenges of business including requests from manufacturers to sell vehicles "at cost" |

| 6. | Does management resist the institutional imperative? | Yes | Yes, management has been disciplined in capital allocate and diversification into related fields such as services, aftermarket and dealership acquisitions |

| 7. | Focus on Return on Equity not Earnings per share | Yes | Company has achieved respectable returns on equity in (15%-18% range), supported by vehicle floor plan financing at attractive rates. We should note that ample capital at low rates may not persist in the long-term future. |

| 8. | Calculates "owner earnings" | Yes | AutoNation generates cash flows in excess of capital requirements. This cash is available for distribution to shareholders or acquisition of tuck-in dealerships |

| 9. | Looks for companies with high profit margins | No | AutoNation is very low margin business with 2% net margin. Majority of profits are made in services and parts, followed by insurance and finance. New car sales are close to "at cost" |

| 10. | For every dollar retained, create at least one dollar of the market value | Yes | Management has been repurchasing shares over the past 3 years at prices above current share price. Generally, it is expected that company's rational capital allocation will result in value creation for shareholders |

| 11. | What is the value of the business? | $48 | Estimate of intrinsic value is in $48 per share range. |

| 12. | Can the business be purchased at a significant discount to its real value. (DCF) | Not yet | Not yet, we'd advise to start adding at prices below $40 a share. Current price is $42.16 |

{kind=link}

0 Comments