Investment Thesis

We’re appraising biopharma and rare disease specialist company, Shire, whose stock is approaching Fat Pitch territory. The stock is trading near 3 year low, with forward Price-to-earnings of 8.5. Fair value estimate is GBP 45-50 a share whilst stock is trading at GBP38 a share, offering 25% margin of safety. With 30% margin of safety, we’re adding to the positions between GBP31-35 per share (vs GBP38 current price).

Shire plc is Dublin based biopharmaceutical company operating in 5 key Genetic Diseases (25% of 2016 product sales), Neuroscience (23%), Hematology (21%), Internal Medicine (16%), Immunology (14%). The headline sales are forecasted at $15bln in 2017.

Focus on rare diseases

Shire’s core therapeutic areas include attention deficit hyperactivity disorder (ADHD), Hemophilia, and Immunoglobulin therapies, coupled with other expanding Rare Disease franchise. These well-defined market segments, protected by significant entry barriers, have enabled the company to secure market shares with dominant high prices, intellectual property, and tightly controlled expenses.

Growth through value creating acquisitions

With its leading position in ADHD attention deficit disorder, niche status in rare genetic disorders along with the acquisitions of Viropharma, NPS Pharma, Dyax Corp, and Baxalta, Shire has grown into a leading biotech pharma company focused on rare diseases, with strong pricing power. Shire maintains a highly acquisitive strategy targeting new therapeutic areas internally and externally.

Patent portfolio

Shire has deftly expanded the patent portfolio through acquisitions and in-house R&D efforts in order to build-up scale in a focused set of therapeutic areas and as a springboard for further product development. The company has built up a diverse portfolio of both small-molecule and biologic products focused generally on niche markets. This diversity allows the company to better withstand specific product risks while using a specialist-focused sales force to penetrate markets, keep expenses down, and maintain strong operating margins.

Vyvanse, the company’s only blockbuster drug with over $1bln sales, has patent protection until 2023; however, as a small molecule it will quickly be genericized when its exclusivity ends.

Underserved market & large runway

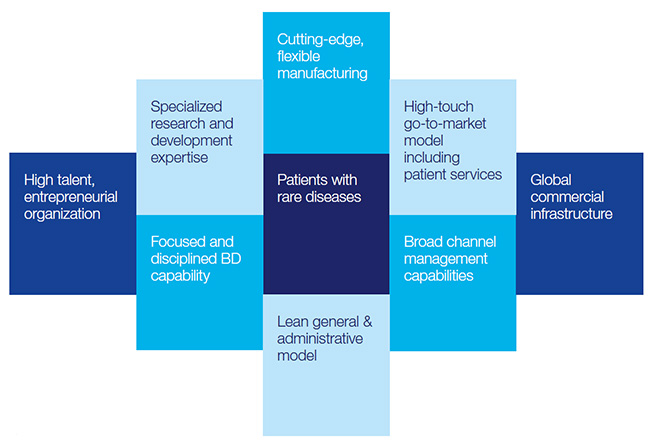

There are over 7000 rare diseases characterized by small number of patients, lacking or non-existent standard of care, little competition from other pharma companies for research, efficient scale opportunity to establish presence and deter future competition.

M&A track record and future M&A opportunity set

Shire’s reliance on acquisitions for growth, as well as an uneven M&A record, makes this an uncertain strategy, as increasing competition for promising products and high valuations for smaller drug-development companies make successful acquisitions increasingly challenging and expensive, weighing on returns on invested capital.

Shire’s reliance on acquisitions for growth, as well as an uneven M&A record, makes this an uncertain strategy, as increasing competition for promising products and high valuations for smaller drug-development companies make successful acquisitions increasingly challenging and expensive, weighing on returns on invested capital.

Efficient scale & Pricing power

By their nature, rare diseases only offer small population of patients, making it less attractive for competing companies to invest in R&D and develop alternative drugs for same or similar indicators, as is often the case for diseases with

By their nature, rare diseases only offer small population of patients, making it less attractive for competing companies to invest in R&D and develop alternative drugs for same or similar indicators, as is often the case for diseases with large patient population. This gives Shire a distinct competitive advantage and pricing power.

Barriers to entry: Baxalta’s dominant hemophilia franchise and plasma-derived proteins–particularly immunoglobulins for rare immunological and neurological disorders–also build on Shire’s rare-disease portfolio, and while Shire is realizing more synergies from the deal than anticipated.

Disruption

Baxalta Hemophilia business is facing upcoming hemophilia competition from Roche (emicizumab) and future gene therapies (from firms such as BioMarin and Spark).

Orphan diseases niche

Shire’s focus on orphan diseases brings about many benefits in form of small patient population, extraordinarily high unmet needs, no or limited established standard of care, few or no effective therapies, very high revenues per patient often in many hundreds’ of thousands of dollars per patient. In order to make drug development attractive, company enjoys sales exclusivity for 7 years in US and 10 years in

Shire’s focus on orphan diseases brings about many benefits in form of small patient population, extraordinarily high unmet needs, no or limited established standard of care, few or no effective therapies, very high revenues per patient often in many hundreds’ of thousands of dollars per patient. In order to make drug development attractive, company enjoys sales exclusivity for 7 years in US and 10 years in EU, and further benefits from accelerated approval processes associated with orphan drug designations.

Sourcing of ideas internally and externally

Shire has historically been open to collaboration and partnering with external research institutions and emerging “start-up” companies for novel therapeutic approaches.

Development and trials

Shire has tailored its R&D organization to grow specialized expertise to address the challenges of developing new medicines in rare disease indications, such as recruiting hard-to-find patients, navigating ill-defined current standards of treatment, and pioneering regulatory pathways. Similarly, once new therapies are approved, Shire can then apply sophisticated approaches to increase diagnosis rates, support patients as they initiate therapy, and productively engage with patients and specialist treatment centers.

Shire has tailored its R&D organization to grow specialized expertise to address the challenges of developing new medicines in rare disease indications, such as recruiting hard-to-find patients, navigating ill-defined current standards of treatment, and pioneering regulatory pathways. Similarly, once new therapies are approved, Shire can then apply sophisticated approaches to increase diagnosis rates, support patients as they initiate therapy, and productively engage with patients and specialist treatment centers.

Baxalta Synergies

Shire is delivering on the Baxalta integration and cost synergies are ahead of expectations. Accelerated synergies have cushioned

Shire is delivering on the Baxalta integration and cost synergies are ahead of expectations. Accelerated synergies have cushioned initial impact of earlier than expected Lialda generic competition. Importantly, strong performance of the Immunology and solid Hemophilia growth underline the quality of the performance.

| Competitive Advantage | Narrow |

|---|---|

| Fair Value Estimate | GBP 4,500.00p - GBP5,000.00p (ADR: $180.00-200.00) |

| Stock Price | GBP 3,807.16p (ADR: $148.61) |

| Fat Pitch Price | GBP 3,150.00p - GBP3.500.00p (ADR: $125.00-140.00) |

| 52 Wk range | 5,377.00p- 3,873.00p (ADR: $147.79 - $209.22) |

| Market Cap. | USD 45.01bln |

| Volatily | Medium |

| Balance Sheet | |

| Shareholder Equity | $31.3bln |

| ROE (%) | 13.8% |

| Net Debt | $21.5bln |

| Debt/EBITDA | 3.1 |

| Potential Appreciation | 25% |

| Dividend Yield (%) | 0.6% |

| PE Data | |

| 2016 | 11.6 |

| 2017 | 9.8 |

| 2018 | 8.9 |

| 2019 | 7.8 |

Fat Pitch Price GBP31.5 - GBP35.5

$15bln annual sales in '17

10% EPS compounded growth between 2016-2021

Latest developments

Shire’s capital allocation priorities for 2018 are investing in organic growth, reducing leverage and dividends. Surplus capital may be deployed for business development or share buybacks. Management expects the immunology franchise to grow ahead of previous guidance of 6-8% for the full year and view 10% growth as achievable. Shire sees consensus forecasts for a ~50% erosion of FEIBA by 2022 (given likely competition from ACE910) as “reasonable” but believe Factor VIII will remain the standard of care in the larger non-inhibitor setting.

Shire continues to expect to deliver year 3 synergies of $700m on an annualized basis. Management sees it as on track to meet its 2-3x net debt to EBITDA leverage by end 2017.

Risks

- Shire’s key drugs are subject to eventual patent expiry, which puts pressure on R&D pipeline to deliver new products or engage in acquisitions to replenish the pipeline.

- Shire is encumbered by $22bln of debt following Baxalta acquisition. Management’s attention remains on maximizing cash flows and paying down debt.

- Future M&A acquisitions may be harder to come back than in the past leading to expensive acquisitions, potential value erosion and/or poor returns on equity

- Congress is reviewing whether existing Orphan drug classification may be creating unintended commercial opportunities for unfair pricing, mistaken misclassification of drugs as orphans and unreasonable sales exclusivity

Durable long-term advantages

- Diversified product base and pipeline

- Industry leading rare disease portfolio with high barriers to entry and pricing power

- Large number (7,000+) of rare diseases with extremely underserved clinical needs

- Small patient population for any given rare diseases with high sales per patient p.a.

- Limited competition and efficient scale for any given rare disease treatment

- Special set of competencies to develop and commercialize rare disease treatments (clinical trials, regulatory approvals, formulary inclusions)

Valuation of existing portfolio of drugs

Based on the valuation of existing marketed products and the minimal value assigned to the future pipeline, fair value discounted cash flow estimate of Shire’s stock is GBP45 per share. The uncertainty in valuing pharma company such as Shire is analyst’s ability to accurately forecast future drug sales, patent expiries, ability to develop and commercialize new therapies and potential erosion of sales to existing drugs from competition. To account for a range of scenarios, we offer a range of reasonable DCF estimates for Shire stock as follows:

- GBP60 per share – optimistic scenario: limited hemophilia competition, continued

- GBP50 per share – base case scenario: modest impact to hemophilia franchise with gradual erosion in mid-single digit % per year from 2019.

- GBP40 per share – pessimistic scenario: strong competition in hemophilia franchise, drug pricing congressional scrutiny resulting more pricing pressure and depressed margins

At the current price of GBP38 per share, a lot of the bad news and potential risks are baked into the share price and investors are paying nothing for any future pipeline breakthroughs, effectively getting the future pipeline for free. We see limited downside to the stock price barring low likelihood-high impact credit type event due to high net debt load.

High leverage (40% of market cap) magnifies any swings in the value of underlying assets. As a rule of thumb, 10% reduction in value of product assets would translate to 15% reduction in DCF estimate per share.

Long term path of $20bln annual sales: Shire’s ambition is to grow sales from $15 billion in 2017 to $20 billion by 2020, around 15% sales CAGR. For 2017, the guidance is 33-36% growth in USD for product revenue and 11-16% rise in EPS as the year is expected to see continuous strong demand for its products coupled with Baxalta’s contribution as well. Shire’s gross margin is high in the industry at 78%, reflecting the premium pricing its niche products enjoy.

High debt levels: After the acquisition of Dyax and Baxalta, net debt rose from USD1.5 billion in 2015 to USD22.4 billion in 2016. This is more than 4x multiple against estimated free cash flow of $4-5bln annually. Considering Shire’s stretched balance sheet coupled with management’s commitment to pay down the debt, Shire will temporary pause on making further acquisitions as it focuses on integrating existing operations.

Spin-off: Management announced a strategic review into the ownership of the Neuroscience division which will include a possibility of a spin-off. Management sees the review as a natural evolution of strategy post-Baxalta and now view Shire as two distinct businesses: rare diseases and neuroscience. The review will be complete by year end.

Bulls Say

- Rare disease portfolio and diversified pipeline makes Shire immune singe-drug patent expiries

- Blockbuster Vyvanse growing in ADHD and eating-disorder indications with strong pricing

- Baxalta’s immunoglobin business is seeing strong demand with high barriers to entry and oligopoly like markets

Bears Say

- Shire is dependent on Vyvanse for sales growth, making the future pipeline big driver of long-term returns. Big launch of lanadelumab (2018) also needs to go right.

- Baxalta’s key hemophilia plasma product Feiba and recombinant Advate are at risk of market disruption from Roche and Alnylam’s strong performing alternatives with little response from Shire

- Large debt levels at $20bln require Shire management to successfully integrate Baxalta, pay down the debt and protect Baxalta’s hemophilia franchise.

- Future acquisitions may be expensive and result in poor returns on capital invested.

{kind=link}

0 Comments