Investment Thesis

American Airlines is one of the largest US domestic carriers.

- Formed after the merger with US Airway, with integration still ongoing

- Shares down 30%, Buffett owns est. $2bln AAL stock as part airlines sector bet, the estimated purchase price is below $40 per share

- Below average profitability (4% of sales vs 10% for leading players) offers an opportunity material increase profits from $2bln to $4bln a year

- High levels of debt due to re-fleeting with new aircraft, although that would help with fuel and maintenance bill (offset by higher depreciation charges)

- Industry running above 80% utilization ratio, indicating rational pricing and rational fleet growth

- Concern remains with ultra low-cost competitors (e.g. Spirit) and highly aggressive international players (e.g. Emirates)

Airlines have suffered between 9%-30% this year on fears of rising fuel cost, which is up 50% in the last 12 months. However, the industry continues to report a healthy load factor above 80%, and disciplined pricing with 60% of fuel increases passed on to the customers.

Industry capacity in a commodity business which competes on price is key to pricing discipline and industry continues to show discipline in managing capacity.

Management continues to prioritize shareholder returns above new capital investments. American Airlines is an exception to this trend as management has embarked on the refleeting drive, which is expected to moderate over the coming 2 years.

Valuations remain low, partly due to investors’ justified scepticism about how long the industry will maintain it’s newly found pricing and capital discipline. It may be that airlines need to survive a full business cycle including a recession and high oil prices for an investor community to change the sentiment.

Airline industry remains very competitive with low barriers to entry outside major hubs (which have to allocate landing slots). Also pricing discipline is hard to maintain as arlines operate with large fixed cost, making it tempting to lower the prices of the marginal seat to fill the plane. Unfortunately, the price of the last seat quickly becomes the price of the first seat.

Due to commodity nature of the industry in which players largely compete on price, the prices are subject to irrational competitive action – effectively the most price aggresive competitor (e.g. airline in bankrupcy protection) sets the price ceiling for the rest.

| Durable Competitive Advantage | None |

|---|---|

| Range of Fair Value Estimate | $40.00 - $70.00 |

| Stock Price | $37.12 |

| Consider Buying Below | $40.00 |

| 52 Wk range | 59.08- 35.64 |

| Market Cap. | $17.4bln |

| Volatily | High |

| Balance Sheet | |

| Shareholder Equity | -$1bn |

| Adjusted ROE (%) | 34.7 |

| Net Debt | $19.1bln |

| Debt/EBITDA | 3.6 |

| Potential Appreciation | 8%-88% |

| Dividend Yield (%) | 1.08% |

| PE Data | |

| 2017 | 9.3 |

| 2018 | 7.7 |

| 2019 | 6.3 |

| 2020 | 5.5 |

Although domestic airline industry has consolidated to 4 big players (American, Delta, United, and Southwest), the industry has a history of fierce price competition, irrational investments in fleet growth, highly unionized workforce and volatile earnings due to fuel fluctuations.

Whilst discipline seems to have come back and consolidation has certainly helped, the emergence of ultra low-cost competition with significant cost advantages, as well as continued high levels of debt make airlines a much riskier investment. High level of margin of safety is required to provide security and safety.

Load factor has been holding up above 80% across the industry allowing management to maintain pricing discipline, generate sufficient cash flows to pay for the investments and service debt. However, an economic recession, demand slowdown, or irrational fleet growth would cause the load factor to drop.

Rising interest rates environment has the potential to increase interest expense on a sizeable debt load ($19bln), which is higher than that market cap ($17bln).

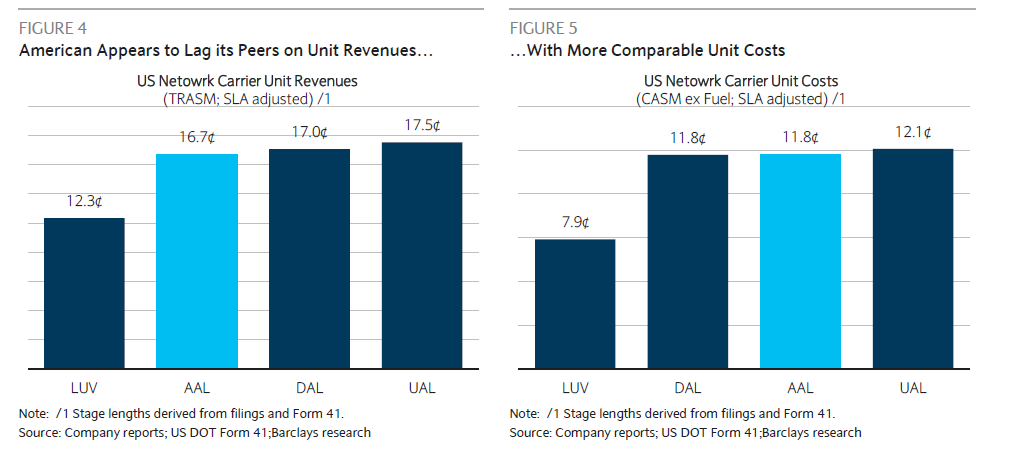

Higher operating cost per available seat mile compared to Southwest and ultra-low-cost competitors will cause AA to cede market share.

Airlines may be unable to pass on fuel and labor cost increases to the customers resulting in margin compression.

long-term BUSINESS QUESTIONS & DYNAMICS

- Q: Would the industry remain profitable? A; Consolidated domestic market with 4 major players instilling pricing and investment discipline. It is likely but not certain that airlines industry will over the next 10

- Q: Will airlines adopt shareholder-friendly policies? A: Present management rightly focuses on profitability, cash generation, and share repurchases rather than growth.

- Q: Will customers continue to fly? A: The US continues to be the largest and most profitable air transport market with some barriers to entry. Demand for flying is set to rise with no close substitute.

- Q: Will American Airlines hold their market share? A: AA has a number of major hubs (Dallas, Charlotte) within their network driving profitable traffic, however higher operating cost and pricing will cause it cede market share to Southwest and ultra low-cost competitors over time.

Valuation

On

The equity value is negative $1bln so valuation based on book value cannot be made.

In terms of free cash flow, AAL generates an operating cash flow of $4bln a year, which is expected to rise to $6bln by 2020 (if company closes profitability gap to Delta/Southwest), whilst capital expenditure is expected to fall from $6bln in 2017 to $3bln in 2020, netting $3bln of free cash flows a year. This compares to the current enterprise value of $28bln ($17bln equity and $19bln debt).

Bulls Say

- Closing profitability gap to Delta (net profit 10% of revenue) would double profitability

- Reduction of debt load would increase market capitalization even without any increase in enterprise value

- Significant share buybacks, Since July 2014 through December 31, 2017, company has repurchased 262.3 million shares of common stock for $10.6 billion at a weighted average cost per share of $40.22, reducing share count by 35% from 752mln to 490mln

Bears Say

- The highest level of debt in the industry at 3.6 net debt/EBITDA including $7bln of pension liabilities, amplifying any underlying deterioration in business performance

- Uncompetitive cost structure at c$11.8 per available seat mile (ASM) vs c$7.9 ASM for Southwest Airlines

- Risk of economic recession & load factor drop, fuel price increases, irrational pricing competition, undisciplined capital expansion

{kind=link}